A subject is considered material if it could substantially affect the organisation’s ability to create value in the short, medium and long-term. DFCC Bank is able to successfully demonstrate its integrated thinking, which is a primary aim of integrated reporting, by highlighting how material matters are connected with its strategy, governance, performance and future prospects. While identifying material matters, the Bank considers financial and non-financial information, as well as their magnitude of effect and likelihood of occurrence. This can be explained as follows:

The Bank has been reaching out to its stakeholders on a continuous basis over the years, to better understand their concerns and the relevance of such issues to their priorities. This covers the economic, environmental, governance, and social issues, in addition to inclusivity. The Bank is of the firm view that stakeholders have the right to be heard, in terms of the impact of various issues on them, and vice versa.

As part of its sustainability practices, DFCC Bank continuously engages with stakeholders with a view to identifying and addressing the following:

- Significant impacts related to business operations and strategy;

- Stakeholders significantly impacted; and

- Stakeholders with significant potential to influence the Bank, its activities, profitability and reputation.

The Bank has identified eight distinct groups as comprising its major stakeholders. These include:

- Investors/Shareholders

- Customers

- Employees

- Business Partners

- Regulators

- Communities

- Advocacy Groups (Media and NGOs), and

- Industry Associations

The external environment includes economic, environment, governance, and social-related trends. The Bank’s Sustainability Strategy and Plan also considers all relevant trends in the external environment, which it considers as being material.

By conducting materiality analysis on a regular basis, DFCC Bank is able to identify and determine aspects that are of importance to the Bank’s stakeholders and to the Bank. This is analysed in terms of its economic, social, and environmental agenda for sustainable value creation.

DFCC Bank has identified the following issues which are of material interest:

- Increased demand for Green Financing (environmentally friendly projects and investments) with sector-specific expertise and has a less harmful impact on the environment, such as renewable energy. This is in alignment with the Government’s policy on conserving the environment, as well as the Bank’s own commitment to environmental stewardship.

- Health and wellness-enhanced productivity, with an emphasis on work-life balance.

- Empowered staff, including special focus on female staff and other vulnerable categories.

- Collaboration and teamwork across functionalities and levels of seniority.

- Enhanced productivity and process efficiencies through investment in staff knowledge and skills (training and knowledge development).

- Increased resource efficiency by decreasing energy and paper usage, minimising wastage, and use of appropriate processes and technologies.

- Healthy and attractive workplace culture that attracts and retains diverse categories of staff, who are able to perform to the best of their ability.

- Clarity on career progression, including mentoring and remedial assistance for those who are slow in their progress.

- Customer-centric services and engagement across all geographic and functional areas.

- Increasingly differentiated and evolving customer needs on financial services, including wealth management advisory services in keeping with international best practices, while considering local requirements.

- New technologies for customer investment and use, e.g. smart/precision agriculture, pollution control, energy efficient technologies, smart buildings, renewable energy, etc.

- Increased demand for convenient, remote, streamlined, and flexible services.

- Increasing demand for new and innovative services which maximise customer convenience and benefits.

- Trend towards purposeful and responsible businesses, which are committed to making a positive impact on society and solving challenges that affect society while also making profits.

- Need to improve financial literacy, especially among vulnerable individuals and communities.

- Specialised MSME services, including non-financial services for capacity and performance enhancement.

- Partnerships and collaborations with professional apex bodies.

- Increasing the involvement of entrepreneurs and MSMEs in creating positive social and environmental impacts.

- Increased use and influence of social media to maximise efficiency of our communications.

- Increased investment in sustainability initiatives, including using less resources, addressing environmental and social impacts, CSR, disaster relief, etc.

- Economic performance in alignment with national policies and priorities.

- Increased demand for transparent reporting on non-financial information including environmental and social issues.

- Compliance with the Sri Lanka Banks’ Association’s (SLBA) Sustainable Banking Initiative (SBI) principles.

- Need to contribute towards UN Sustainable Development Goals (SDGs).

- Implementing suitable initiatives to counter the negative outlook in the banking sector.

- Being adaptable to an increasingly competitive business environment.

- Building resilient business strategies, including sustainability.

- Sustainable sourcing and supply chains.

- Decent work and fair remuneration for all categories of workers.

- Entrepreneurial skills training for the self-employed.

- Education and skills building opportunities, with reskilling and upskilling where required.

- Taking measures to respond to the increased frequency and scale of natural disasters, poor preparedness, and response times.

- Reducing environmental and negative social impacts from economic activities, and raising awareness of same among all stakeholders.

- Increasing the importance of organisational reputation as a competitive advantage.

- Taking suitable measures regarding the declining trends in exports.

- Need to improve business resilience.

- Use of new technologies, e.g. Digitisation, Artificial Intelligence, Machine Learning, Robotic Process Automation, etc.

- Growth of MSMEs.

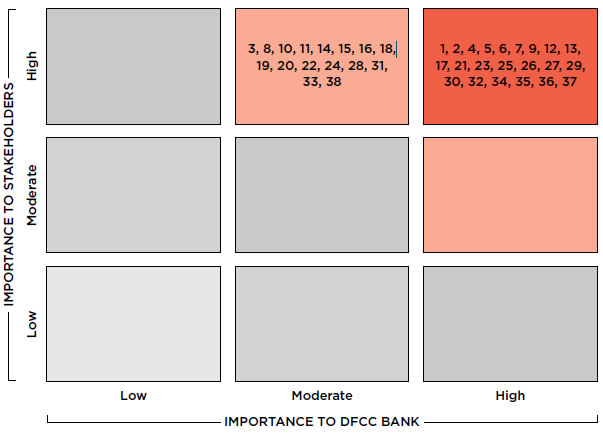

These trends have been mapped on the GRI Standards two-dimensional matrix:

The Bank’s Sustainability Strategy and Plan is based on the Materiality Matrix with stakeholder priorities duly considered during their implementation.

Management Approach

The Bank makes every effort to engage with each group of stakeholders in order to map out its portfolio of activities. By aligning its activities with the needs of each group of stakeholders, the Bank is able to generate and deliver value to its stakeholders and derive value from them in return, thereby maximising the benefits accruing to all. This will result in achieving the Bank’s two-fold objectives, namely:

- Strategic goal:

- ensuring the credibility of the Bank’s sustainability plans and its operations.

- Relationship goal:

- understanding and building close relationships with customers.

- empowering employees with rewarding careers.

- generating steady returns for investors.

- establishing mutually beneficial and profitable partnerships.

- acting responsibly towards society and the environment.

The Bank determines materiality issues through the process of a materiality analysis, whereby the relevance of each issue or trend is apportioned to different stakeholder groups. This is explained by means of the following table, which describes the relevance and applicability of trends from 2021 to the Annual Report of 2022:

| Materiality Trends from 2021 | Relevant for 2022 Annual Report | Key Stakeholder Group |

| 1. Increased demand for Green Financing | Yes | Customers |

| 2. Health and wellness-enhanced productivity | Yes | Employees |

| 3. Empowered staff, with special focus on female empowerment | Yes | Employees |

| 4. Collaboration and teamwork | Yes | Employees |

| 5. Enhanced productivity, process efficiencies and investments in training and development | Yes | Employees |

| 6. Increased resource efficiencies | Yes | Investors and shareholders |

| 7. Healthy and attractive workplace culture | Yes | Employees |

| 8. Clarity on career progression | Yes | Employees |

| 9. Customer-centric services and engagement | Yes | Customers |

| 10. Increasingly differentiated and evolving customer needs on financial services, including wealth management and advisory services | Yes | Customers |

| 11. New technologies for customer investment and use | Yes | Investors and shareholders |

| 12. Increased demand for convenient, remote and streamlined services | Yes | Customers |

| 13. Increased demand for innovative services | Yes | Customers |

| 14. Trend towards purposeful and responsible business | Yes | Communities |

| 15. Need to improve financial literacy | Yes | Communities |

| 16. Specialised MSME services, including non-financial services | Yes | Communities |

| 17. Partnerships and collaborations with professional apex bodies | Yes | Industry Associations |

| 18. Increasing entrepreneurs and MSMEs involvement in creating positive social and environmental impacts | Yes | Communities |

| 19. Increased use and influence of social media | Yes | Investors and shareholders |

| 20. Increased investment in sustainability initiatives | Yes | Communities |

| 21. Economic performance | Yes | Investors and shareholders |

| 22. Increased demand for transparent reporting | Yes | Regulators |

| 23. Compliance with Sri Lanka Bank’s Associations and Sustainable Banking Initiative Principles | Yes | Regulators |

| 24. Need to contribute towards UN SDGs | Yes | Communities |

| 25. Negative outlook for the banking sector | Yes | Investors and shareholders |

| 26. Increasingly competitive business environment | Yes | Investors and shareholders |

| 27. Building resilient business strategies | Yes | Investors and shareholders |

| 28. Sustainable sourcing and supply chains | Yes | Business Partners |

| 29. Decent work or fair waged jobs | Yes | Employees |

| 30. Entrepreneurial skills training for self-employed | Yes | Communities |

| 31. Education and skills building opportunities | Yes | Communities |

| 32. Increased frequency and scale of natural disasters and poor preparedness | Yes | Communities |

| 33. Environmental and social impacts from economic activities | Yes | Communities |

| 34. Increasing importance of organisational reputation | Yes | Investors and shareholders |

| 35. Declining trends in exports | Yes | Investors and Shareholders |

| 36. Need to improve business resilience | Yes | Investors and Shareholders |

| 37. Use of new technologies i.e. digitisation | Yes | Customers |

| 38. Growth of MSMEs | Yes | Customers |

Materiality Matrix

A few key stakeholder groups have no material matters mapped on to them. It is because the Bank first identifies its key stakeholders, and their stakeholder concerns by filling the Stakeholder information table above in the Stakeholder section.

The Management Discussion and Analysis section in this Annual Report will include details and analyses of the initiatives undertaken by the Bank during the period under review, in terms of various materiality issues.