Strategic Direction and Outlook

Formulating a viable and sustainable strategic direction in the financial sector in Sri Lanka has become increasingly difficult, due to the current state of the economy, as well as the constantly changing and unpredictable external environment. Scenario planning has emerged as an onerous task, given the volatile situation, and the continually evolving consumer preferences. Fast-advancing technological frontiers, in addition to the profusion of hi-tech financial solutions, which can satisfy latent or even emergent consumer needs, add to the complexity. It is this altered environment, and DFCC Bank’s response, that is being analysed in this section.

Adapting to a Transformed Landscape

DFCC Bank, in common with the banking industry in general, has been operating under a fundamentally transformed landscape during the year under review. The sheer magnitude of economic turbulence has been unprecedented, mainly caused by the knock-on effects of the Covid-19 Pandemic such as default on foreign debt, and the resultant disruptions to the financial sector and the economy. The banking industry was particularly hit, due to its pivotal role in the country’s economy, leading to a cascading effect upon other sectors. Consequent to the prevailing instability, banks had to face the issue of deteriorating credit quality, and distressed customers who were struggling to overcome the scarcity of essentials and unrelenting inflation.

The resultant funding pressures and tighter liquidity conditions have inevitably affected lenders. The industry is currently faced with the looming threat of a haircut on domestic debt, as a result of the Government’s negotiations with overseas institutional creditors, and the envisaged structural reforms. In such a scenario, investments in local sovereign debt instruments are likely to be impacted. Prevailing interest rates will also limit the inflow of funds into the banking sector, as customers may seek higher returns on their investments through government securities offering more attractive rates.

Given the need to accumulate a large scale of capital required to support long term asset growth, and exorbitant risks inherent in considerably expanding the loan book in such trying circumstances in the coming years, DFCC has had to revisit previously relied upon assumptions. As the country is still in the early stages of its economic recovery, a number of important underlying factors in the economy and the banking industry could remain unchanged in the foreseeable future. In this highly demanding and risk-prone environment, DFCC has been compelled to take stock of its previous medium-term vision, using it as a blueprint to review the limits of its feasibility in realising growth-oriented goals. The Bank is in the process of formulating a new medium-term plan in 2023, once the economy and financial market show signs of stabilising. The specifics of the plan will depend on the outcome of the government’s negotiations with the IMF and other creditors.

Negotiations with overseas creditors, under the aegis of the Paris Club, are progressing smoothly, with France playing a pivotal role in ensuring their successful conclusion. Over and above the USD 2.9 Bn pledged by the IMF, a final agreement could go a long way in restoring the credibility of Sri Lanka in the eyes of the international investors and business community, paving the way for additional financing from countries and institutions.

Currently, the primary focus of DFCC Bank is to fortify and strengthen the balance sheet, preserve and enhance capital and liquidity, and grow profitability. Following the hike in SDFR and SLFR policy interest rates and spike in yields of government securities, the Bank’s liability mobilisation would be a costly exercise, due to the high costs associated with deposits and borrowings. In addition, the industry has to face the reality of competing for funds which show an increasing tendency towards moving into more attractive government securities offering higher rates, the risk of a possible domestic debt restructuring is a further threat faced by the banking sector.

Borrowers are in a distressed situation due to the overall slump in economic growth, inflation which is still at a high level, and considerable increases in lending rates. Targeted lending to selected sectors will be possible only if such sectors show signs of healthy growth prospects, which appears unlikely in the current scenario. The entire banking sector is grappling with deteriorating credit quality, making it crucial to manage the lending book and asset quality.

The shortage of US Dollars and the resultant drop in imports has impacted the earning of net fees and commission incomes through trade. The forex crisis has also effectively halted imports of motor vehicles and other capital goods, which were a lucrative source of income for the Bank.

Due to the curtailment of banking limits arising from the sovereign credit rating downgrade, engaging in correspondent banking has been restricted. Facing such economic realities require DFCC to approach the coming quarters with caution. Possible key focus areas for the coming year include: mitigating and minimising impairments, expanding the deposit base at rates that are as competitive as possible, conscientiously and prudently lending to selected segments such as the export sector, generating transaction volumes to grow fee and commission income, reversal of impairments and proactively managing operating costs.

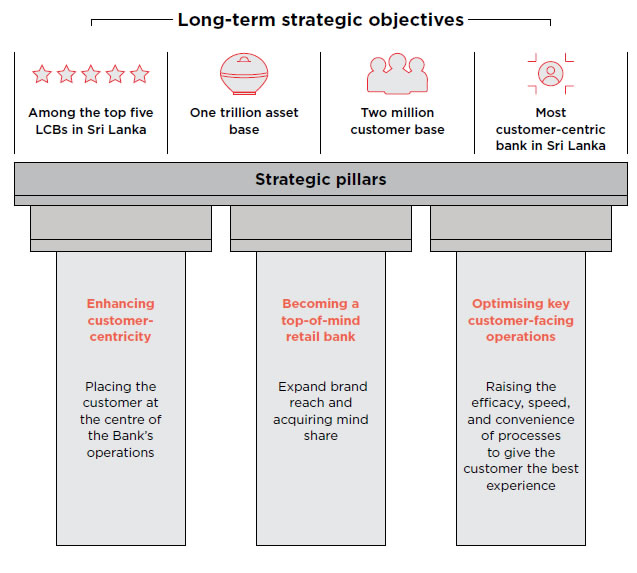

While a new medium-term plan for the organisation is to be developed afresh in 2023 given the new realities, a key long term strategic objective will still remain unchanged – the pursuit of becoming the most customer-centric bank by being data driven and digitally enabled.

War Rooms

This concept enabled the Bank to overcome the travails of the pandemic with relative ease, and speed up the digitisation process across the board. In the present context, War Rooms have been revived as part of the preparations to navigate the prevailing tough realities, and introduce a series of actionable initiatives in the near term. These shall form the launching pad for sustained efforts to realise strategic priorities in the medium to long term. Dedicated War Rooms have been operationalised across Deposit Mobilisation, Cost Management, Fee Income and Impairment Management.

Deposit Mobilisation

Securing low-cost funding is one of the most attractive options to enhance the Bank’s financial stability and augment its funding operations, although the prevailing high interest regime is a constraining factor. Strengthening the liability base will be a source of considerable support to the balance sheet position, improved liquidity and lending capacity. Strong retail funding will keep the balance sheet on a sound footing in the near-term and beyond.

Cost Management

Managing costs is being implemented through a holistic effort which encompasses reducing waste, improving processes, and raising productivity. This has become an organisation-wide priority in efforts to limit costs, relative to income growth. While improving efficiency contributes more towards increasing profitability, when combined with reducing waste, it also complements DFCC’s sustainability initiatives. For instance, trackers are used to monitor progress in terms of rationalising the usage of paper and energy, which provides an actionable metric which can be used to monitor usage.

Fee Income

As this particular source of income has been adversely impacted by the economic conditions, the Bank has adopted a focused approach to driving product lines that generate higher fee and commission income, such as trade products, exchange conversions, digital platforms and promotion of cross-selling.

Impairment Management

During an economic downturn, managing impairment can become a serious issue with dire consequences. The Bank has adopted a system of centralised monitoring and follow-up through the Head Office and recovery hubs across the regions. Non-performing clients are dealt with proactively in order to arrive at mutually beneficial compromises in a timely and efficient manner.

Outlook

Despite overwhelming odds, DFCC Bank is confident of achieving its objectives during the coming year. This confidence stems from its financial and managerial strengths, proven record of resilience in adversity, commitment of its talented team of staff members, as well as the trust and loyalty of the customer base over the past 67 years.