We are pleased to present our 10th Integrated Report in accordance with the International <IR> Framework of the IFRS Foundation. This Report has been prepared for the purpose of communicating DFCC Bank’s strategy, governance, performance and prospects, in the context of its external environment, leading to the creation of sustainable value for its stakeholders in the short, medium and long-term.

Reporting Period and Boundary

Scope and Boundary

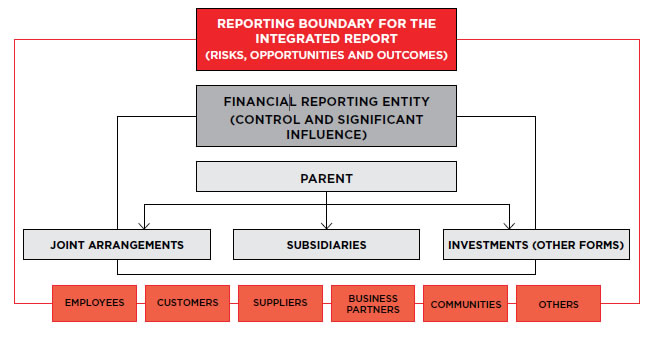

The DFCC Bank PLC Annual Report 2022 is a reflection of the Bank’s integrated approach of management from 1 January 2022 to 31 December 2022. The scope of our reporting covers DFCC Bank PLC (“DFCC Bank” or “Bank”) and the DFCC Bank Group (“Group”) comprising the Bank and its subsidiaries, a joint venture company, and an associate company. The respective entities have been duly identified where applicable.

This Report also communicates the full range of factors that materially affect the Bank’s ability to create value over time, with special emphasis on non-financial factors such as Social and Relationship, as well as Natural Capitals. This highlights the Bank’s unwavering focus and commitment to people and the natural environment, which extends to all entities covered in this Report.

This Annual Report is available as:

Financial Reporting Boundary

This is in alignment with our financial statements reporting boundary and includes DFCC Bank PLC and its subsidiaries. In the process of choosing the stakeholders and entities to be included in this Annual Report, we have based our decision on the <IR> Framework depicted below:

Entities/stakeholders considered in determining the reporting boundary

Integrated Reporting Boundary

The guiding principles in integrated reporting have been taken into consideration in the preparation and presentation of the report. These are based on the International <IR> Framework 2021 of the IFRS Foundation. This includes material risks, opportunities and outcomes attributable to or associated with; operating environment, our value creation model, and capitals.

Standards, Principles, Guidelines and Protocols

We have strived to deliver a comprehensive, balanced and relevant Report adhering to the accepted Key Standards, Principles, Guidelines and Protocols.

Compliance

The Board of Directors of DFCC Bank accepts responsibility for the veracity and accuracy of the entirety of this Annual Report 2022, in the spirit of good governance. The information contained herein has been prepared in compliance with all applicable laws, regulations, and standards, which are declared on pages 172 to 178 of the Annual Report. This Report has been prepared in accordance with the following:

Statutory Frameworks

- Companies Act No. 07 of 2007

- Sri Lanka Financial Reporting Standards

- Listing Rules of the Colombo Stock Exchange

Financial Frameworks

- Sri Lanka Accounting Standards (LKASs/SLFRSs) issued by the Institute of Chartered Accountants of Sri Lanka

- Banking Act No. 30 of 1988 and amendments thereto

- Companies Act No. 07 of 2007

Reporting Frameworks

- GRI Standards

- The International <IR> Framework

- Smart Integrated Reporting MethodologyTM

- Sustainability frameworks

- GRI Standards issued by the Global Sustainability Standards Board (GSSB)

- Sustainable Banking Principles of Sustainable Banking Initiative by the Sri Lanka Banks’ Association

- The United Nations Sustainable Development Goals and the United Nations Global Compact Principles

- The Sri Lanka Sustainable Banking Principles (SBP)

- Protocols – The Greenhouse Gas Protocol Corporate Standard published by the World Resource Institute (WRI) and the World Business Council for Sustainable Development (WBCSD) is used to measure and report on the Bank’s carbon footprint.

Corporate Governance

Governance, Risk Management and Operations

- The Companies Act No. 07 of 2007

- The Listing Rules of the Colombo Stock Exchange (CSE)

- Code of Best Practice on Corporate Governance issued by the Institute of Chartered Accountants of Sri Lanka

- Banking Act Direction No. 01 of 2016 on Capital Requirements under Basel III and amendments thereto

- Banking Act No. 30 of 1988 and amendments thereto

- Securities and Exchange Commission of Sri Lanka (SEC) Act No. 19 of 2021 including directives and circulars

- Banking Act Direction No. 11 of 2007 and subsequent amendments thereto

- Directions issued by the Central Bank of Sri Lanka and the Basel Capital Accord (III)

- Listing Rules of the Colombo Stock Exchange (CSE).

Assurance

The necessary assurance has been provided by KPMG Sri Lanka on the Financial Statements, including the notes to the accounts. As provided in paragraphs 2.17 and 2.18 of the <IR> Framework, organisations are not required to adopt the Framework’s categorisation of capitals. Thus the capitals have been categorised in a manner that best describes the Bank’s value creation process.

Precautionary Principle

The precautionary principle, proposed as a guideline in environmental decision making, has four central components: taking preventive action in the face of uncertainty; shifting the burden of proof to the proponents of an activity; exploring a wide range of alternatives to possibly harmful actions; and increasing public participation in decision making.

On the basis of this principle, we are aware of, and take responsibility for the social and environmental consequences of our actions, both direct and indirect. We acknowledge that the environmental consequences of our actions are of greater significance as a result of our lending operations, which we have taken care to address and mitigate through credit policies, post-disbursement supervision, and risk management processes.

Determining Materiality

The interpretation of materiality varies across report forms due to differences in audience, purpose and scope. In Integrated Reporting, a matter is material if it could substantively affect the organisation’s ability to create value in the short, medium and long term. The process of determining materiality is entity specific and based on industry and other factors, as well as multi-stakeholder perspectives.

DFCC Bank is able to successfully demonstrate its “Integrated thinking” by highlighting how material matters are connected with its strategy, governance, performance and future prospects. The Bank also considers financial and non-financial information, as well as their magnitude of effect and likelihood of occurrence, when determining materiality. Stakeholders with significant potential to influence the Bank, its activities, profitability and reputation are also considered.

The Six Capitals in Value Creation

The International Integrated Reporting Council (IIRC) recognises six distinct but interrelated capitals: Financial, Manufactured, Natural, Human, Intellectual, and Social and Relationship. Integrated Reporting is based on the understanding that future cash flows and other conceptions of value are dependent on a wider range of capitals, interactions, activities, causes and effects, and relationships than those directly associated with changes in financial capital. The concept of value includes: (a) value to the organisation, and (b) value to society/stakeholders, including the environment. At DFCC Bank, we regard these capitals as inputs to create value for stakeholders, which are considered an output.

Capitals Discussed in the DFCC Bank’s Annual Report

This Report showcases Social and Relationship Capital, as being distinct from Natural or Environmental capital due to the following:

- In terms of the Triple Bottom Line concept, on which DFCC Bank bases its sustainability strategy, Social and Relationship Capital relates to People, while Natural Capital relates to the Planet

- Stakeholders for both these Capitals are mostly from different categories, though there is a certain level of overlap

- As a financial organisation, our impact on both is entirely different. While our actions have a direct impact on People, they tend to affect the Planet to a lesser degree, and indirectly through our lending activities

DFCC Bank has a stated goal of becoming carbon neutral by 2030. This is achievable with a combination of energy conservation, renewable energy, and purchasing of carbon offsets over time. Technological advances and changing economic policies could have a positive impact on achieving this goal.

For any clarification on this report please write to:

The Company Secretary

DFCC Bank PLC

73/5, Galle Road, Colombo 3, Sri Lanka

Email: info@dfccbank.com

Company Secretary

Ms N Ranaraja

Registered Office

73/5, Galle Road, Colombo 3, Sri Lanka

Phone: +94 11 244 2442

Fax: +94 11 244 0376

Email: info@dfccbank.com

Website: www.dfcc.lk