Financial Performance Overview

During the year under review, DFCC Bank remained committed to providing high-quality, customer-centric banking services across the country, despite facing unprecedented challenges and a volatile economic environment. As a result of this dedication, the Bank’s performance remained strong and resilient, though relatively modest compared to previous years.

This can be attributed to three contributory factors that had a combined cascading effect across the economy. Firstly, the foreign exchange crisis caused by the lingering effects of the pandemic, as tourism had come to a standstill, export earnings dwindled, and inward remittances reduced to a trickle. The second was the devaluation of the Sri Lanka Rupee (SLR) which led to runaway inflation and widespread economic hardship. The third and most important factor was the high interest regime, which impacted the entire economy while the banking sector was particularly hard hit.

In line with the Bank’s corporate strategy and its stated goal of becoming one of Sri Lanka’s most customer-centric, digitally enabled bank by 2025, a new T24 Temenos Core Banking System was implemented on 21 October 2021, along with a feature-rich online banking platform. This transition has resulted in an improved, digitally enabled banking service that is highly flexible, agile, and highly beneficial to customers.

The year saw an adverse impact on profitability due to increased impairment costs and provisioning. However, this situation should improve as impairment mitigation measures take further effect over the upcoming quarters. The fiscal policies of the Central Bank of Sri Lanka (CBSL) will support the impacts of already implemented tight monetary policy measures, preventing the buildup of aggregate demand pressures and anchoring inflation expectations, which will help to bring down headline inflation and support the economy in achieving its potential. The domestic banking system’s foreign exchange liquidity has also shown some improvement due to increased inflows of export proceeds and workers’ remittances. Collectively, these measures and impacts could help to build momentum for economic recovery in 2023.

The Bank implemented several concessionary schemes to support customers affected by the pandemic, helping them to emerge stronger, through numerous moratoriums, relief measures and advisory support and services, in accordance with the directives issued by the Central Bank of Sri Lanka.

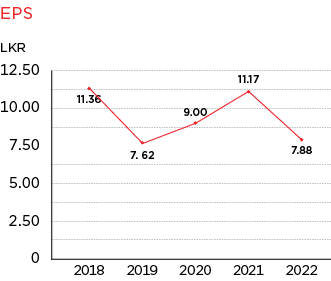

The Bank’s total assets grew by LKR 80,421 Mn, representing a 17% increase from December 2021. This growth included a loan portfolio increase of LKR 3,172 Mn, bringing the total to LKR 369,072 Mn, compared to LKR 365,901 Mn as of 31 December 2021, which represents a 1% increase. The Bank’s deposit base increased to LKR 370,314 Mn as of 31 December 2022, compared to LKR 319,861 Mn as of 31 December 2021, reflecting a 16% increase. The Bank’s CASA ratio, which indicates the proportion of low-cost deposits, decreased to 18.50% by 31 December 2022, compared to 31.25% in December 2021. The Bank’s profit after tax decreased by 22% to LKR 2,513 Mn, and the earnings per share (EPS) decreased by 33% during the year 2022.

Income Statement Analysis

Profitability

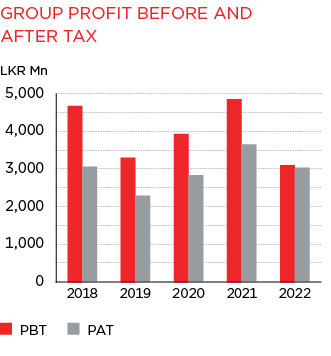

DFCC Bank PLC, the largest entity within the Group, reported a Profit Before Tax (PBT) of LKR 2,439 Mn and a Profit After Tax (PAT) of LKR 2,513 Mn for the year ended 31 December 2022. This compares with a PBT of LKR 4,326 Mn and a PAT of LKR 3,222 Mn in the previous year.

The Group recorded a PBT of LKR 3,112 Mn and PAT of LKR 3,042 Mn for the year ended 31 December 2022 as compared to LKR 4,859 Mn and LKR 3,665 Mn respectively in 2021. All the member entities of the Group made positive contributions to this performance.

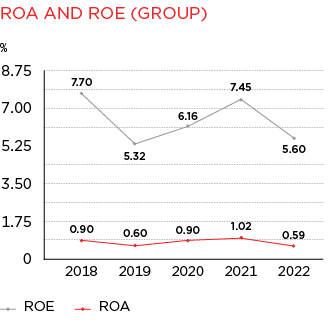

The Bank’s Return on Equity (ROE) declined to 5.04% during the year ended 31 December 2022 from 6.55% recorded for the year ended 31 December 2021. The Bank’s Return on Assets (ROA) before tax for the year ended 31 December 2022 is 0.46% compared to 0.92% for the year ended 31 December 2021.

Net Interest Income

The tight liquidity conditions in the domestic money market have resulted in continuously rising market interest rates. As a result, the Bank’s deposit and lending products experienced a significant increase in interest rates during the period under review. While the higher interest rates may have depressed the lending portfolio, it led to an overall improvement in Net Interest income (NII). In fact, the NIIs of the entire banking sector have grown dramatically due to the high lending rates.

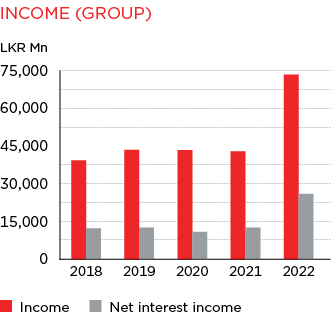

The Bank’s Net Interest Income (NII), which is its core business, increased by 106% to reach LKR 26.0 Bn by the end of 2022. The interest margin increased from 2.66% in December 2021 to 4.96% by December 2022, due to a 1,985 bps increase in the AWPLR over the past 12 months and the time lag in repricing existing deposits.

Fee and Commission Income

The untiring efforts of the Bank’s staff led to an increase in non-funded business during the year, resulting in a rise in net fee and commission income to LKR 2,877 Mn for the year ended 31 December 2022, compared to LKR 2,596 Mn in the previous year.

Although trade operations were severely impacted in the early part of the year, they improved to a certain extent as more foreign funding became available. Additionally, inward remittances significantly improved enabling the Bank to accommodate more trade operations. Fee based business have shown a slight improvement in profitability due to the higher tariffs levied, though the actual volume of operations is lower than before.

Fees generated from loans and advances, credit cards, and fees collected from trade accounted for the majority of the fee and commission income.

Other Comprehensive Income (OCI)

Changes in fair value of investments in equity securities and fixed income securities (treasury bills and bonds) and movement in hedging reserve are recorded through OCI. Due to the application of hedge accounting, the impact on equity due to changes in foreign currency rates was minimised. A fair value loss of LKR 4,506 Mn was recorded on account of equity securities outstanding as at 31 December 2022.

Impairment Charge on Loans and Other Losses

The impaired loan (Stage 3) ratio increased from 3.03% in December 2021 to 4.36% as at 31 December 2022. In order to address the current and potential future impacts of prevailing economic conditions on the lending portfolio, the Bank has made adequate impairment provisions during the year, by introducing changes to internal models to cover unseen risk factors in the present highly uncertain and volatile environment.

The main uncertainties regarding the recoverability of the Bank’s total sovereign debt exposure relate to the debt service capacity of the Government of Sri Lanka. This is, in turn, affected by the development of the prevailing macroeconomic environment as well as the levels of liquidity of the Government. The ongoing debt restructuring negotiations with the International

Monetary Fund (IMF) and the resultant comprehensive debt restructuring programme could have other adverse outcomes. Based on the currently available data, the Bank has used its discretion and informed judgment to estimate the recoverable value. Accordingly, it has been decided to maintain a minimum impairment provision cover of 35% of our overall sovereign debt investment.

With these provisions made to cover the additional risk in the economic environment, the impairment charge recorded an increase of 280% against the comparative period and stood at LKR 17 Bn for the year ended 31 December 2022 compared to LKR 4.5 Bn in the comparable year.

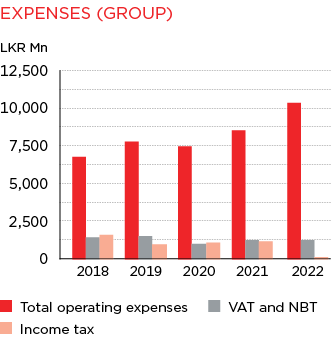

Operating Expenses

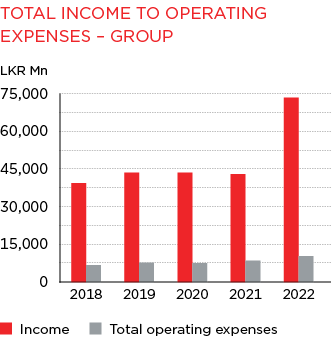

With the implementation of the core banking system during the last quarter of 2021, the Bank upgraded its IT infrastructure to provide multiple channels for service delivery to customers through a robust digital drive. Due to the increase in IT related expenses as a result of infrastructure upgrades carried out, and increases in cost due to inflation and SLR devaluation, the operating expenses for the year ended 31 December 2022 increased to LKR 10,117 Mn compared with LKR 8,381 Mn during the corresponding period in 2021. However, the numerous process automation and workflow management systems introduced during the period helped curtail and manage operating expenses at reduced levels.

Profit After Tax (PAT)

The Bank recorded a PAT decrease of 22% to LKR 2,513 Mn for the year 2022 compared to LKR 3,222 Mn in 2021. The Bank’s total tax expense, which includes financial services VAT and income tax is LKR 1,179 Mn for the year ended 31 December 2022. As a result, the Bank’s tax expense taken as a percentage of operating profit for the year stood at 31.94%.

During the year there were revision to the tax legislations applicable to the Bank. Value added tax rate was revised to 18% effective from 1 January 2022. An additional tax charge of LKR 43 Mn in the year was attributable to the 2.5% Social Security Contribution Levy (SSCL) on value addition effective from 1 October 2022. The Bank computed the income tax liability for the first six months of the year of assessment 2022/23 by applying the income tax rate of 24% and the revised income tax rate of 30% for the balance six months. Inland Revenue (Amendment) Act no 45 of 2022 was considered to calculate the income tax liability for the second six months of the year of assessment. The deferred tax assets/liabilities of the Bank as at 31 December 2022 were computed using the revised income tax rate of 30%.

A newly introduced one off surcharge tax of LKR 1,232 Mn was paid by the Bank, calculated at 25% of the taxable income for the year of basement 2020/2021 and was directly set off against the opening equity in line with the Statement of Alternative Treatment (SoAT) on accounting for the surcharge tax issued by The Institute of Chartered Accountants of Sri Lanka.

Financial Position Analysis

Assets

Despite the challenges faced by the economy and the banking sector, DFCC Bank’s total assets increased by LKR 80,421 Mn, recording a growth of 17% from December 2021. This constitutes a loan portfolio growth of LKR 3,172 Mn to LKR 369,072 Mn compared to LKR 365,901 Mn as at 31 December 2021, an increase of 1%. The Bank did not pursue an aggressive lending growth strategy due to high inflation, currency depreciation and a rising interest rate environment. The Bank curtailed its foreign currency lending portfolio significantly during the year ended 31 December 2022.

The Bank has implemented several relief schemes in line with the Central Bank of Sri Lanka’s directives to support those affected customers. The Bank’s net asset value per share was recorded at LKR 125.96 as at 31 December 2022 compared with LKR 152.83 recorded as at 31 December 2021.

Liabilities

The liabilities increased by 18% over the previous year to LKR 515,205 Mn as at the year end. The Bank’s deposit base also experienced a growth of 16%, recording an increase of LKR 50,453 Mn to LKR 370,314 Mn from LKR 319,861 Mn as at 31 December 2021. This resulted in recording a loan to deposit ratio of 108%. Further CASA ratio is 18.5% as at 31 December 2022. Funding costs of the Bank were also contained by using medium to long-term concessionary credit lines. When these concessionary term borrowings are considered, the CASA ratio further improved to 22.21% as at 31 December 2022.

DFCC Bank continued its approach to tap local and foreign currency related, long-to-medium-term borrowing opportunities.

Equity and Compliance with Capital Requirements

DFCC Bank’s total equity increased to LKR 50 Bn as at 31 December 2022 with the recorded profit after tax of LKR 2.5 Bn.

With the objective of assisting the future asset growth of the Bank and to improve the capital ratios of the Bank, the Board of Directors have decided to issue up to eighty million (80,000,000) Basel III compliant, subordinated, listed, rated, unsecured, redeemable debentures with a non-viability conversion option, each at an issue price (par value) of LKR 100 with a term up to seven years’ subject to obtaining all necessary regulatory and other approvals.

As at 31 December 2022 the Bank recorded Tier 1 and Total Capital ratios of 10.085% and 13.148% respectively. The Bank’s Net Stable Funding Ratio (NSFR) was 126.55% and Liquidity Coverage Ratio (LCR) – all currency was 202.34% as at 31 December 2022. All these ratios were maintained above the minimum regulatory requirement.

Credit Quality

Following the Bank’s prudent lending policies, it did not pursue aggressive growth particularly in sectors that exhibited stress. During the year, the Bank had a moderate growth in its loan book covering corporate, retail, and small and medium size business segments. The expansion into new geographical areas and new customer segments increased the challenge to maintain a sustainable risk profile. The Bank continued to improve its pre and post credit monitoring mechanisms through changes to internal processes and timely actions. This has brought positive results in maintaining credit quality amidst the stressed economic situation.

Dividend Policy

The banking industry faced many challenges during the year from both the business and regulatory fronts due to the global pandemic. The adverse business environment caused constraints for the growth of returns on equity. The minimum capital requirements became more stringent with the adoption of BASEL III. The Bank’s dividend policy seeks to maximise shareholder wealth whilst ensuring there is sufficient capital for expansion as it leverages its island-wide presence and investments in technology. Accordingly, the Board of Directors has approved a final dividend of LKR 2.00 per share in the form of a scrip dividend for the year ended 31 December 2022, balancing the needs of shareholders with business plans. Accordingly, the dividend payout ratio for the year ended 31 December 2022 is over 33% on the distributable profit.

Group Performance

The DFCC Group consists of DFCC Bank PLC and its subsidiaries; DFCC Consulting (Pvt) Limited, Lanka Industrial Estates Limited (LINDEL), Synapsys Limited, its joint venture company Acuity Partners (Pvt) Limited (Acuity), and its associate company National Asset Management Limited (NAMAL). LINDEL is a 31 March reporting entity whilst the others are 31 December reporting entities. For the purpose of consolidated financials, 12 months results from 1 January to 31 December 2022 were accounted for in all Group entities. Financials of the 31 March entity were subject to a review by its External Auditor covering the period reported.

The Group made a profit after tax of LKR 3,042 Mn during the year ended 31 December 2022. This is compared to LKR 3,665 Mn made in the year 2021. DFCC Bank accounted for majority of the Group profit with profit after tax of LKR 2,513 Mn, while LINDEL (LKR 224 Mn), Acuity Partners (LKR 332 Mn), Synapsys (LKR 56 Mn), and DFCC Consulting (LKR 24 Mn) contributed positively by way of profit after tax to the Group. In the previous year, Synapsys, Acuity Partners, DFCC Consulting, and LINDEL reported profit after tax of LKR 1.7 Mn, 293 Mn, LKR 5 Mn, and LKR 238 Mn respectively. The associate company, NAMAL, contributed LKR 0.74 Mn to the Group, a decrease from LKR 3.8 Mn in the year 2021. An Inter-company dividend of LKR 90 Mn was paid to DFCC Bank by LINDEL.

![]()

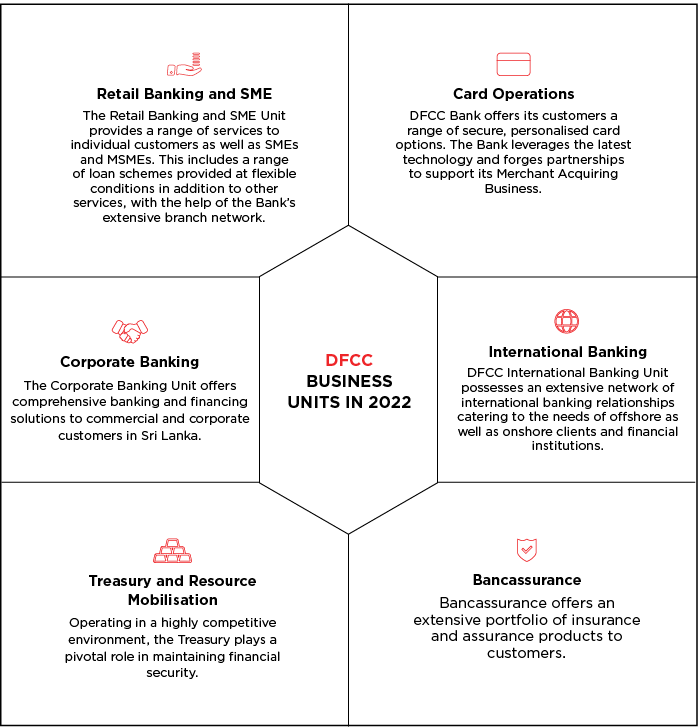

Retail Banking and SME

Liabilities

Regulator mandated high interest rates resulted in an exponential growth of 21.5% in the liability base over 2021. The Bank focused on growing its retail liabilities while broad-basing the clientele by reaching out to hitherto untapped segments, including a renewed focus on women’s banking propositions.

Campaigns and Initiatives

The regulatory mandate that prevailed during the year enabled the Bank to introduce special Fixed Deposit (FD) rates for 100, 200 and 300-day deposits while an extra special rate was offered for five-year FDs. A competitive rate was also offered for foreign currency deposits in a bid to attract much-needed FOREX liquidity to the country. These initiatives were underpinned by a Mega Street Campaign that was conducted island-wide.

DFCC Junior Campaigns at selected schools augmented the Bank’s commitment to education, and gearing up the next generation to become future leaders.

Deposit Champions were appointed per Branch while a specialised team addressed the Current Account Transaction operation related issues. The Deposit Rate App Sheet speeded up the approval process and turnaround time to the customer. Encompassing the diversity of the customer base in its core value, the Garusaru Gift Scheme was streamlined to ensure that benefits to senior citizens were duly granted.

M-Teller

M-Teller collections doubled in 2022 over 2021 and the staff attached to the Deposit Mobile Teller (DMT) unit increased from 45 to 75. Average transactions per month increased by 74% while the average value per transaction increased by 60%. Similarly, a 48% increase was seen in this average collection per M-Teller.

Outlook for 2023

The economic downturn resulted in heightened NPL factors on several fronts as consumers battled to balance their budgets between the rising cost of living and loan servicing. Given that, the Bank has offered a great deal of flexibility and support to its customer base in these turbulent times. In 2023, CASA will be a key focus area of the Retail Banking arm, in order to meet the versatile needs of the growing customers. The propositions and the savings products will be revamped with enhanced features and benefits. Year round attractive card deals and promotions will be offered to increase the card base while increasing the card holder’s spending.

Export financing will also be a key focus area in attracting foreign currency to the country. We will continue to promote credit schemes with the assistance of ADB, CBSL (GOSL), DFC, etc, while enhancing service offerings with the launch of SME propositions to facilitate SME growth.

We are committed towards continuous improvement on service efficiencies to provide unmatched customer experience.

![]()

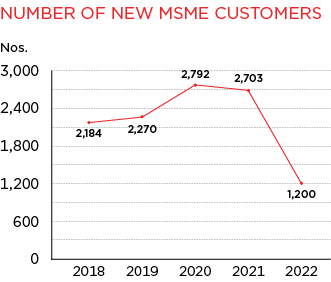

MSME Sector

In the downward economic trend of the year under review, it was the medium to small enterprise sector that was gravely and adversely impacted, given their business model and their limited resources. Recognising the need to offer the segment relief, the Bank initiated a loan restructuring programme and a debt moratorium, which greatly benefitted the impacted group.

The Bank offers a range of products to suit different segments of the MSME sector, which are;

- Sahaya Small Business Loans

- NCRCS and SAPP Refinance Loans for the agriculture sector

- Supplier Financing Schemes

- Ethera Saviya Loan Scheme – for skilled migrants

- Bio Gas Loan Scheme – as a solution to the energy crisis and fertiliser crisis

- Leasing.

Female Empowerment Through the MSME Department

Currently, over 40% of the MSME customer-base represents women entrepreneurs mainly engaged in sectors such as tea, dairy, crop farming, mini garments and beauty culture. ADB funded loans under concessionary rates were disbursed among the women led enterprises. DFCC Aloka is specifically designed to support women entrepreneurs to launch mainstream business.

DFCC Aloka Initiatives

Several programmes were carried out by DFCC Aloka that provided a special platform for the women entrepreneurs to network with each other while serving the community.

International Women’s Day

An informative and an exciting event was carried out on 8 March 2022 to commemorate International Women’s Day, attended by Aloka customers and staff members. CEO Thimal Perera addressed the gathering emphasising the Bank being an equal opportunity employer while Aloka offers women the opportunity to engage in their businesses with ease.

The number of participants was limited due to residual pandemic issues and the event was aired on the DFCC YouTube channel, LinkedIn and Facebook pages facilitating many viewers to be part of the programme.

“Avurudu Kumari”

Selecting manufacturing plants regionally across the island, DFCC Aloka crowned the Avurudu Kumari, sponsoring the Avurudu celebrations at those locations.

“Visit Kandy” Promotional Campaign

DFCC Bank partnered with “Visit Kandy 2022” organised by the Kandy City Centre to coincide with the Dalada Perahara as the Official Banking Partner.

Providing yet another opportunity for the MSME customers, four customers from the Katugastota Branch were selected to participate in the event. The campaign was held from 10-13 August at the KCC lobby and the customers displayed their products such as apparel, jaggery, leather products, and spices in their stalls. MSME officers actively participated in the event along with staff members from the branches in the Kandy Region.

Galle District Women Chamber of Commerce AGM 2022

The Galle District Women Chamber of Commerce (GDWCC) concluded its AGM on 27 August 2022 with the participation of over 100 female entrepreneurs from all walks of life. DFCC Galle branch and DFCC Aloka took the initiative to partner this event by sponsoring it, creating visibility for the Bank in the Galle Town.

WCIC Women Entrepreneur Awards 2022 Powered by DFCC Aloka

DFCC Bank partnered with the Women’s Chamber of Industry and Commerce as the Platinum Sponsor of WCIC Women Entrepreneur Awards 2022, powered by DFCC Aloka.

Workshop for MSME Women Entrepreneurs in Kurunegala

DFCC Bank organised a workshop on entrepreneurship development for small and medium scale women entrepreneurs in and around the Kurunegala area. The workshop was successfully held on 19 March 2022 at the Hotel Indoora, Kurunegala with the participation of over 75 women entrepreneurs. The programme provided training for the participants on record keeping, financial management, entrepreneurship, networking and marketing, including digital marketing tools, as well as value-added food processing. The training was delivered by Dr Rukmal Weerasinghe, Chairman, Centre for Entrepreneurship and Innovation of the University of Sri Jayewardenepura and Ms Nirmala Wijeratne, of Sunshine Food and Creations.

The sessions were well received and appreciated by the participants and the Bank is pleased of this contribution to a segment that is increasing in volume and growth.

Partnership with Durdans Hospital to Offer Exclusive Medical Benefits to Aloka Customers

This allows exclusive medical packages at attractive discounts to the DFCC Aloka customers, who will be entitled to discounts on dental procedures, cosmetic procedures, and room rates on hospitalisation.

Partnership with AMRAK Institute of Medical Sciences to Extend Special Discounts to Aloka Customers

Selected top achievers will be awarded fully sponsored scholarships through this scheme.

DFCC Aloka Sponsored WCIC Santa’s Village

DFCC Aloka supported yet another initiative by the Women’s Chamber of Industry and Commerce, encouraging and supporting female entrepreneurs across the island by facilitating the “Santa’s Village” – a Christmas fair.

DFCC Aloka Pocket Campaigns

The branch network conducted over 300 pocket campaigns at Regional and Branch level to take the DFCC Aloka female centric savings account to all Sri Lankan women across the country.

Introduction of the Biogas Project for Dairy Farmers

A partnership was formed with the National Innovation Agency (NIA) to promote biogas technology to create awareness on sustainable alternative energy sources. Through this partnership, DFCC Bank has provided a special loan product to purchase biogas technology for dairy farmers. The Bank has planned to conduct a series of awareness campaigns targeting the dairy farmers based in the North-Central Province.

Outlook for 2023

In the year 2023, the Bank plans on exerting greater efforts in promoting the refinance and subsidy schemes financed by multiple funding agencies such as CBSL (GOSL), ADB and IFAD to provide lending to the agricultural, manufacturing and services sectors. It also plans to introduce a digital ecosystem to assist the farming community and agribusinesses to develop their entrepreneurial skills, in addition to providing sustainable marketing, supply chain, and payment solutions.

![]()

Credit Cards and Merchant Acquiring Business

The card issuing business made good progress in 2022. The cards in force grew steadily, cardholder spend increases were seen across daily essentials and the portfolio grew at a formidable pace. Several card promotions were introduced to spur spending and new products such as; Aloka debit/credit card for females and a new partner was added to the Affinity credit card product. With the current economic trends, the Bank introduced a number of controls to mitigate the risk with a focus on improving credit quality.

The Balance Build Up Products were curtailed and certain relaxations were introduced during the fourth quarter keeping the seasonal spend in mind. Throughout the year a variety of promotions were introduced, whether at popular outlets, travel and holidays or via online portals to cater to the spending patterns of the customers. The Back to School Easy Payment Plan was relaunched to assist parents pay school fees and a first of its kind seasonal promotion in Sri Lanka the “Make a Wish” campaign was launched targeting new card acquisitions and spend.

Similarly, the sales volume of the Merchant Acquiring Business increased rapidly as the Bank focused on using this channel to improve CASA balances and it was complemented with a significant number of new merchants being acquired. The Bank partnered with JCB to accept international cards via DFCC ATMs, while UnionPay card acceptance was enabled at point of sale machines. The need for development of digital-based solutions and expansion of e-commerce resulted in the launch of two major Internet Payment Gateways, Mastercard Payment Gateway and Paycorp. The Mastercard Payment Gateway Service platform enabled the acceptance of digital transactions through Visa and Mastercard whilst Paycorp allowed the acceptance of American Express, UnionPay and Diners cards through Paycorp Payment Gateway Services Platform. An aggregator arrangement was established to offer Easy Payment Plans on websites.

Outlook for 2023

The Bank will focus on key projects such as achieving Payment Card Industry Data Security Standards compliance, Visa, UnionPay and Mastercard acceptance on ATM’s, migration to a new debit card switch and enabling Application Programming Interface (API) access for QR transactions on point of sales machines and websites. Further, introducing new Affinity partners will be taken forward with the issuance of new co-branded credit cards.

![]()

Bancassurance

Forging relationships with customers, offering them tailor made products in their lifetime and ensuring their loved ones are supported in case of an eventuality, are done with great care and thought by the Bank, through its Bancassurance channel offered at affordable group rates to its customer base.

The partnership formed with AIA Insurance in 2016 continues to add value to the customer base as the range of life insurance products offered to them has widened to include education protection for children, in these difficult times. Together with the addition, the Bancassurance product currently includes an attractive suite, to cater to the diversified needs of the customers.

Life Insurance Products

1. AIA Easy Pensions Plus*

A pre-packaged retirement plan with the option of selecting from 6 packages at the customers’ convenience. An in-built Life Benefit is available in each package along with an Accident Benefit. Also, AIA will continue the policy by paying premiums on behalf of the customer, if the customer passes away or becomes totally and permanently disabled. The pension fund will be boosted with a Loyalty Reward of up to 8 times (800%) of the Annualised Basic Premium. Further, customers can choose to receive the Maturity Benefit as a lump sum or as a monthly pension or as a combination of both.

2. AIA Smart Pensions Plus*

A comprehensive pension plan with the choice of selecting the pension fund at maturity as a lump sum or as a monthly income or as a combination of both. AIA will continue the policy by paying premiums on behalf of the customer, if the customer passes away or becomes totally and permanently disabled. A professionally managed pension fund increased further by a loyalty reward up to 1,650% of the Annualised Basic Premium. Customers have the ability of adding the optional benefits such as Accident Benefit, Critical Illness Benefit, Permanent Disability Benefit, Adult Surgery Benefit, Hospitalisation Benefit, Health Expense Cover, etc.

3. AIA Health Protector*

A worldwide coverage on hospitalisation expenses up to LKR 50 Mn which allows the best healthcare in the world. AIA Health Protector provides the convenience of cashless hospitalisation at over 60 hospitals in Sri Lanka and overseas. Further, this gives coverage for 37 illnesses including cancer, stroke, heart attack and kidney failure and worldwide coverage for 250 surgeries and 136 one-day surgeries. Inbuilt benefits such as coverage for wellness, dental, maternity and hospitalisation in ayurvedic hospitals are also available. This includes an in-built Life Benefit and Accident Benefit so that customers can enhance the protection of their loved ones.

4. AIA Suwa Diriya*

A life insurance plan which provides coverage for 4 major common critical illnesses (heart, cancer, kidney failure and stroke). This covers a specific set of minor heart related illnesses, surgeries and early-stage cancer. Also, “Recovery Benefit”, which provides a monthly income during the recovery phase of a critical illness (in the event of a claim due to major heart disease, major stage cancer, stroke or kidney failure).

5. AIA Super Protector*

A personalised solution with affordable premiums for the protection needs of all Sri Lankans. This provides the ability to select a Life Benefit between LKR 1 Mn to LKR 500 Mn whilst the Life Benefit increases by 5% at each Policy Anniversary (on a simple straight-line basis) until the end of the Policy Term or until a death claim is made. AIA Super Protector has 6 optional benefits to select in order to customise the protection (Accident Death Benefit, Permanent Disability Benefit, Family Income Benefit, Critical Illness Benefit, Returning of Premiums Paid Benefit and Premium Protection Benefit).

6. AIA Education Plan*

A life insurance product specifically designed to safeguard children’s education dreams. AIA Education Plan has a fund that will earn dividends each year so that the education fund continues to grow over time. This also includes an in-built Life Benefit and an Accident Benefit so that customers can enhance the protection of their loved ones. The education fund will be boosted by adding loyalty rewards up to 400% of the Annual Basic Premium on the tenth policy anniversary.

7. AIA Smart Wealth*

A life insurance product specifically designed to create, manage and protect the wealth of Sri Lankans. AIA Smart Wealth provides a long-term protection for a short premium paying term or a single premium. This has a unique dividend system that ensures continuous growth of the fund each year with the ability to claim the fund at maturity as a lump sum or as a monthly income or as a combination of both. The in-built Life Benefit can be selected of up to 50 times the Total Annualised Premium. Moreover, AIA will continue the policy by paying premiums on behalf of the customer, if the customer passes away or becomes totally and permanently disabled.

8. AIA She Protect*

AIA She Protect is a comprehensive life insurance plan, specially designed to protect Sri Lankan women. This is a personalised solution with affordable premiums for women’s protection needs along with the ability of customising the protection with 6 optional benefits that cater to individual needs and expectations.

These long term insurance products are issued and underwritten by AIA Insurance Lanka Limited (AIA Sri Lanka) and offered to the customers of DFCC Bank through the Bancassurance partnership DFCC Bank has with AIA Sri Lanka.

*Please refer the policy document for more details on benefits, applicable terms and conditions, exclusions, etc.

General Insurance

Bancassurance includes a provision of general insurance packages that serve professionals, SMEs and segments of the large corporates supporting the businesses with a long term vision.

Motor insurance includes a private car, commercial vehicle, motorcycle and trade plate insurance, while Fire and Engineering Insurance includes, a Private Dwelling and House Fire Insurance, Commercial Fire Insurance, Plant and Machinery and Contractors All Risk Insurance.

Customer centricity being the core concept, the Bank facilitates this repertoire of tailor made products to its customer base through its insurance service provider, such as, Title, Travel, Surgical, Workmen’s Compensation, General Accidental, Fidelity Guarantee, Marine Imports, Marine Exports, Marine Goods in Transit, Marine Open Cover, and Hull Insurance.

Bancassurance Income Generation

Bancassurance business generated LKR 210 Mn net income for the year 2022. The Gross Written Premium (GWP) generated under General insurance business stood at LKR 1 Bn, while Life insurance premium stood at LKR 400 Mn, (ANP – Annualised New premium). The bancassurance business facilitated claims worth of LKR 226 Mn in 2022 which accounted for 436 cases.

Initiatives

In the year under review, the Bank launched the “Banca Champion” Campaign, the revamped CEO Club 2022, digital lead-generation application, SMS campaigns and social media campaigns on Life Insurance products. An inter-branch competition was launched under the theme, “Bancassurance Retail Challenge” and an island-wide “Banca-Month” programme too was conducted successfully in the third quarter of 2022. An Executive Development Programme for selected DFCC staff was conducted by PIM – Sri Lanka, as part of raising the skills of staff under the DFCC-AIA partnership during 2022.

![]()

Corporate Banking

Expertise across diverse industry sectors, the ability to structure large and complex deals and long-term customer relationships underpin our position as a leading Corporate Bank in the country. The Corporate Banking Unit’s portfolio comprises multinationals, large corporates, middle market enterprises, public sector organisations, as well as non-banking financial institutions. The ability to deliver value in a timely, effective, and industry-specific manner has garnered over 500 corporate customers for the Unit, as of 2022.

Harnessing the resources of a cross-functional team of highly experienced and qualified personnel, the Unit offers a range of solutions to its customers. These include: working capital financing, trade finance, project and term funding, cross-border financing, corporate financing and investment banking, in addition to liquidity and cash management solutions.

Performance in 2022

Overcoming the obstacles that have beset the Sri Lankan economy in general and the banking industry in particular, the Corporate Banking Unit performed significantly well, including consolidation in its asset growth and impairment management. The unit recorded a CASA ratio of 32% as at end December. Operating Income of LKR 6.1 Bn was achieved despite pressure on income of both funded and non-fund bases due to various concessions given during the year and due to the prevailing economic conditions. Strong focus on supporting the exporters, Trade Finance and Cash Management, focus on fee based income, on-boarding quality premium segment customers, cross-selling and focus on profitability enabled the Unit to record sustainable revenue and portfolio growth.

Outlook for 2023

Sri Lanka’s economy is expected to face challenges, based on the envisaged debt restructuring programme, implementation of structural reforms, privatisation of loss-making State-Owned Enterprises, and economic adjustment programmes supported by the International Monetary Fund (IMF). Anticipated growth in the tourism sector, improvements in exports and inward remittances, as well as the Government’s focus on increasing Foreign Direct Investments are likely to positively impact economic growth. The Unit will focus on maintaining asset quality, managing impairments and driving CASA and fee based revenue. Propositions are in place for relationship management, promoting transaction banking and improving process efficiencies to ensure sustainable growth of the business. Aligning with the overall growth strategy of the Bank, Non-Funded Income (NFI) remains a key focus area.

Trade Finance for exporters, working capital, and sustainable finance will be key focus areas for 2023. In partnership with the Banks’ joint venture, Acuity Partners, the Unit will look to support customers with Corporate Finance and Investment Banking services as well. As mentioned above, the Unit will continue to focus on driving CASA, especially the acquisition of operating and current accounts of customers by leveraging the Payments and Cash Management proposition which was voted by customers as the Market Leader and Best Service in Cash Management for 2022 in a survey conducted by the prestigious Euromoney Magazine.

![]()

Treasury

DFCC Bank’s Treasury function is structured on three Pillars: the Front, Middle and Back Offices.

The Treasury Front Office (TFO) is the main income generating unit. The TFO, which comprises a highly experienced team of dealers, generate revenue through trading in foreign exchange and fixed income securities, income through customer-related transactions and interest income from investment. The Unit also manages the Bank’s liquidity ratios and other key regulatory ratios. The TFO reports directly to the Head of Treasury. Treasury Middle Office (TMO) independently reports to the Chief Risk Officer (CRO). TMO engages in risk monitoring and reporting of TFO activities on the basis of Board-approved limits, controls and regulatory guidelines. Treasury Back Office (TBO) comes under the purview of the Head of Finance/Chief Financial Officer (CFO). TBO is responsible to prepare, verify and settle all transactions carried out by the TFO.

Performance in 2022

The Treasury Unit was able to contribute significantly to the Bank’s bottom line under extremely challenging macro and micro environments. Customer related transaction volumes were impacted due to tough economic conditions. The continuation of the economic crisis suppressed potential revenues. Despite these challenges, Treasury was able to deliver a seamless service to the customers through the use of digital channels while ensuring the said revenue targets were achieved.

During the latter part of 2021, DFCC Bank was able to raise long term funding of USD 150 Mn from the United States International Development Finance Corporation at very competitive terms. The Treasury Department was able to successfully hedge the proceeds of the same enabling on-lending to SME, MSME and Women led enterprises at concessionary rates while ensuring steady revenue streams throughout the year.

Outlook for 2023

It is expected that the economic conditions will improve in the coming year. The Treasury Department of the Bank is confident that it will be able to capitalise on the market opportunities.

![]()

Investment Banking

Previously known as the “Resource Mobilisation Unit”, the unit was renamed in 2022 as the Investment Banking Unit to reflect its expanded role within DFCC. In a volatile market, the Investment Banking Unit is well-equipped and highly skilled to offer the customer quick turnaround times with flexible documentation optimising customer benefits in a timely manner.

The Unit continued to manage the Bank’s Quoted share portfolio which is booked under Fair Value through Other Comprehensive Income (FVTOCI) and Fair Value through Profit and Loss (FVTPL) in a profitable manner despite the overall market losing over 30% (All Share Price index) during the year.

In the year 2022, LKR 3,620 Mn was raised through a Rights Issue strengthening the Capital ratio of the Bank.

With customer-centricity as its primary focus, the Unit engages in sourcing medium to long term funding, managing the Bank’s Equity and Unit Trust portfolios, Margin Trading Business, and the Underwriting Business, while acting as the coordinating point for matters relating to Capital Raising and National and International Ratings for the Bank.

On the Margin Trading Portfolio, the existing customers continue to hold the limits with reduced exposure in order to strengthen their portfolio to the high volatile market conditions. We are confident that with the expected improvement in the stock market conditions the clients would enhance their positions according to their capacity and borrowing power.

Outlook for 2023

The Bank will continue sourcing funds from domestic and external channels to support the growth plans. Custodian Banking Services are planned to be launched in 2023. The Bank is confident that the Sri Lankan Equity market will have a steady growth in the coming year.

Trade

In an operating environment that continued to impact imports adversely, the Bank pivoted its operating model and focused on growing the available opportunities and exploring untapped market segments, to maximise its trade business.

This strategy worked well, as by the end of October 2022, the fee income generated from trade business surpassed LKR 800 Mn, which is a contribution of 35% of the overall fee income of the Bank.

Initiatives

To achieve this, the Bank took a number of initiatives including the signing of a Memorandum of Understanding (MOU) with the National Chamber of Exporters and the publication of DFCC advertorials in their quarterly magazine, thereby heightening the Bank’s visibility among the relevant trade groups.

The volatility of the market and economic trends were minutely scrutinised by the team at Trade Business Development Unit that made timely visits to potential business segments while speedily tapping into the cinnamon exporters segment where increased activity was shown.

The challenges are yet to abate to a level where import activities could resume at a reasonable level, given the scarcity of foreign exchange. Facing headwinds with commitment and diligence, the Bank is confident that the Trade business will experience a revival at a higher level, when the economy stabilises to a reasonable position as expected in the year 2023.

Institutional Business Development

Several new corporate relationships were secured by the Institutional Business Development Unit in 2022 that added strength to the Bank’s institutional business portfolio.

In its relentless efforts to be customer-centric, the Bank partnered with the Ceylon Petroleum Corporation (CPC) with collection accounts, where the CPC’s supply chain could deposit funds directly and place orders for their fuel consumption. This initiative significantly eased the burden on the Bank’s customers during the acute fuel shortages as well as the Bank’s collections achieving a significant improvement within a short timeline.

Taking a futuristic view, the Unit entered into strategic business partnerships with institutions such as the Ceylon National Chamber of Industries (CNCI), Industrial Development Board (IDB), Sri Lanka Association for Software Services Companies (SLASSCOM), and the National Innovation Agency (NIA) during the year, which was mutually beneficial for all concerned.

Outlook for 2023

While enhancing opportunity in the businesses onboarded in 2022, the unit will be focused on new tie ups to increase collection, FCY with offshore banking and BOI registered companies and sustainable business in 2023.

Lanka Money Transfer

DFCC Bank has accomplished remarkable growth in LMT (Lanka Money Transfer) for the year 2022 despite the adverse socio-economic conditions that prevailed in Sri Lanka. As of December 2022, the Bank achieved a total of 36,135 transactions with a healthy turnover of USD 39.278 Mn.

Despite unfavourable political, social and economic conditions, the Bank was able to achieve notable results, as the strategies adopted during the crisis paid off in the long term. The Bank sought to support Sri Lanka’s efforts to increase foreign remittances by offering a cash reward scheme in the generation of foreign exchange through authorised banking channels.

Further, the Bank successfully launched a pre-departure loan to overseas job seekers to pay off their visa fee, ticket cost and agency fees. The placement of staff members in UAE and Israel have paid off in increasing the Bank’s market share.

![]()

International Trade and Remittances

DFCC Trade and Remittances Department consists of four units namely Imports, Exports, International Remittances and Correspondent Banking. This structure ensures efficient delivery of services to internal and external customers of the Bank. Apart from the above, the operational functions of Lanka Money Transfer, which handles worker remittances brought into the country, are executed by the Trade and Remittances Department.

Confidently Facing the Headwinds

Even though the negative impact to the economy from the pandemic started to reduce gradually during 2022, the political instability and regulatory restrictions imposed to curtail foreign currency outflow, resulted in a considerable setback for the import and remittance business. Furthermore, defaulting repayment of sovereign debts and downgrading of the country’s credit rating by the international credit agencies was an added burden on an already fragile economy which created obstacles in facilitating trade transactions through global banks.

Notwithstanding this crisis and resultant setbacks, the Bank facilitated many Foreign Currency transactions for our customers. While attending to our customers import requirements, the Bank was also able to facilitate importation of food items, pharmaceuticals and petroleum products which contributed towards fulfilment of the country’s essential import requirements.

Due to the nature of the tasks carried out, such as examining physical documents and issuing the same to customers, the Trade and Remittances Units require physical presence of staff at the office premises and any delay could cause financial losses to customers. Therefore, even with the difficulties experienced in transportation due to scarcity of fuel, the department ensured availability of sufficient staff at office in order to provide uninterrupted services to the Bank’s customers.

The Correspondent Banking Division played a commendable role in strengthening the existing relationships and onboarding new correspondent relationships with international banks, at a time when the country was faced with issues due to defaulting of sovereign debts and downgrading of the Country’s national rating. This timely act of the Correspondent Banking Division was very important to us since global trade transactions were faced with many hindrances due to the prevalent economic constraints of the country.

Despite the above setbacks, the Trade and Remittances Unit helped the Bank generate LKR 1.106 Bn and to achieve the fee and commission income allocated to the trade business. The International Remittance Unit was able to generate LKR 559.76 Mn which is a significant increase in fee and commission income compared to the previous year.

Outlook for 2023

The Trade and Remittance department consists of experienced and committed staff equipped with the required knowledge, and will continue to provide necessary guidance and customised solutions thereby assisting the local businesses expand globally, contributing to the growth of the country’s economy.